FAQs

We have a list below of the most common questions we get asked about personal injury law

Sorry, no FAQs were found.

General Frequently Asked Questions

A significant number of claims resolve by agreement either prior to commencement of court proceedings or during court proceedings. Probably only 1% of claims will end up being heard and determined by a Judge in Court.

You will only need to give evidence if you cannot reach agreement and the judge needs to determine the claim.

The law of negligence in NSW is now modified by the Civil Liability Act 2002 (NSW).

An essential element of negligence is the existence of a duty of care. The courts over the years have accepted categories of duty of care, or that a special relationship exists between parties, that a person must take reasonable care to avoid acts or emissions which are likely to injury another in such a relationship.

Examples would be an employee and an employer, an occupier and an entrant upon premises, a doctor and patient, a school and its students. These are the most common categories.

In most cases there is little issue that a duty of care exists as most injuries would fall under an accepted category where a duty exists.

The Civil Liability Act then sets out three (3) conditions that must exist before negligence arises.

A person is not negligent in failing to take precautions against a risk of injury unless:

- It was a risk of which the person knew or ought to have known

- The risk was not insignificant

- A reasonable person in the circumstances would have taken those precautions

When considering these matters the court must take into account the following:

- The probability of the harm occurring if care were not taken

- The likely seriousness of the harm

- The burden of taking precautions to avoid the risk of harm

- The benefit to society of the activity that creates the risk of harm

Each case is determined on its own facts and circumstances applying the principles as we have outlined above.

The law of negligence is complex and you will need the assistance of a Lawyer who is an expert in personal injury law to advise you whether or not you have a claim for compensation under the Civil Liability Act.

To receive compensation you must notify the person you believe has been negligent and is responsible for the injury you have sustained and advise them that you wish to make a claim for compensation.

In the vast majority of claims the injury will be covered by insurance and you will receive a response from an insurance company to your claim.

You can then negotiate, with the assistance of a Lawyer, the resolution of your claim directly with the insurance company or if you are unable to reach an agreement you must commence a claim for compensation in an appropriate court of NSW.

Compensation under a claim for negligence is called Damages.

Damages are broadly defined to include any form of monetary compensation.

Damages usually include monetary compensation in the form of:-

- Non economic loss which means a lump sum amount for pain and suffering and loss of enjoyment and expectation of life.

- Economic loss which is compensation awarded for loss of income such as wages and payment of medical expenses.

Damages are payable at the conclusion of a negligence claim as a lump sum amount for both economic and non economic loss sustained as a result of the injury.

There are 2 broad types of compensation payable:

- Non-economic loss.

- Economic loss.

Non-economic loss

Non-economic loss includes compensation for pain and suffering, discomfort, inconvenience, loss of pleasure derived from work, hobbies and sport, marriage and child bearing, loss of independent, curtailment of life, loss of expectation of life and disfigurement.

You are entitled to receive a lump sum amount of compensation for non-economic loss as determined by a table under the Civil Liability Act in NSW, Your injuries are compared to that of a most extreme case and you are awarded an amount of money based on what percentage of a most extreme case your injury is compared to a most extreme case. The maximum amount payable under the Civil Liability Act is $551,100.00 for 100% of a most extreme case.

Economic loss

Economic loss covers the loss of the following:

- Past and future loss of income.

- Past and future payment of medical expenses.

- Past and future loss for the capacity to care for oneself and dependants.

- Loss of superannuation entitlements.

Payment of compensation or damages is made as a once off lump sum amount at the conclusion of a civil liability claim. The nature and extent of your injuries and how they affect you on a day to day basis will determine the amount of compensation you are entitled to receive.

Negligence claims are finalised by one of two ways:

- Agreement with the negligent party (or its insurer) or;

- An order of a NSW court.

It is normal to give notice of a claim for negligence to the party you consider has been negligent and to negotiate with them (or usually the insurer) a resolution of the claim prior to the commencement of court proceedings. Often claims can be resolved by agreement with an insurance company prior to commencing any court proceedings.

If, however you are unable to resolve a claim by way of agreement then you must file a claim in a NSW court which has jurisdiction to deal with your matter.

Filing a Statement of Claim in the Court commences a formal claim and will after about 10 months (if you have still not been able to reach an agreement) determined by a Judge. The Judge will hear all the evidence and determine if the defendant was negligent, and if so, how much compensation you are entitled to receive.

Yes. There are various time limits depending on the type of negligence claim and how you are injured. Time limits vary considerably depending on the type of matter such as motor vehicle accidents, work accidents, medical negligence claims and public liability claims.

As a broad rule, you should commence a claim within three years from the date of the accident. However, the law is not so straight forward. The three-year period begins and ends at different times for different types of accidents.

For some types of claims there are also preliminary steps that must be taken before you can claim.

For example, to make a claim for a motor accident you must notify the police within 28 days of your accident and then you must lodge a claim form within six months.

For a work accident, you need to notify your employer immediately and lodge a claim within 28 days.

For some other types of negligence claims, you have three years from the date of “discoverability”. That is, the date which you knew or ought to have known that you had a right to make a claim.

For negligence claims, there is also a 12 year long stop limit which means that after 12 years, you can no longer claim.

The law in relation to time limits is as you can see, complex. If you do miss a time limit you can sometimes get an extension of time to commence proceedings from the court. Again, the rule is different depending on the different type of accident you may have.

The best thing to do is to be aware that time limits do exist and to contact a Lawyer who specialises in personal injury as soon as possible if you think you may have a claim.

If you need assistance or would like further information on the Civil Liability Act in NSW, please do not hesitate to contact us as follows;

- Complete our FREE case assessment form HERE

- Email us at

- Give us a call on (02) 8518 1120

Yes you can however you are likely to obtain significantly less compensation then had you retained the services of an expert Personal Injury Lawyer.

A Lawyer who is a specialist in the area of personal injury law will have great experience in dealing with insurance companies and be able to advise you as to the type of compensation you are entitled to receive as a result of your injury and how much compensation is reasonable and fair.

Most claims resolved by people who are not represented by a Lawyer are resolved for usually about 20% of their real value. You should never speak to an insurance investigator without speaking to a Personal Injury Lawyer first. Anything you say to an insurance investigator can and will be used against you. You must be very careful with your words which can be twisted by an insurance investigator.

You should never negotiate a resolution of your claim without speaking to a Personal Injury Lawyer as you will get much less and any settlement will end your rights to compensation for ever so you need to make sure you are getting the best result you can.

It is important to engage, at an early stage, in any claim an experienced Personal Injury Lawyer and particularly a Lawyer who is an accredited specialist in personal injury law by the Law Society of NSW.

Worker’s Compensation Frequently Asked Questions

If you have been unable to reach agreement with the insurer on the percentage whole person impairment (WPI) your lawyer will make an Application to the Personal Injury Commission (PIC) to appoint an independent medical specialist to assess the percentage WPI.

SIRA is the State Insurance Regulatory Authority (the old Workcover) and is a statutory authority and is therefore under the control of the NSW State Government. Its primary objective is to regulate and oversee the Workers Compensation system in NSW.

SIRA collects all workers compensation premiums, and they are responsible for the payment of workers compensation benefits. It appoints scheme agents (insurance companies such as QBE, Employers Mutual, GIO, etc.) to act as claims handlers on behalf of SIRA. These scheme agents work as claims handling agents on behalf of SIRA. Any benefits which are paid by the scheme are paid by the NSW government, not the scheme agent.

SIRA has a supervisory role over the scheme agents and regularly reviews claims to ensure the scheme agents are correctly applying the law.

The Work Health and Safety Act NSW 2011 (WHS Act) creates a duty on an employer to notify WorkCover immediately if any of the following occur in the workplace:

- The death of a person

- A serious injury or illness of a person

- A dangerous incident

An employer must notify WorkCover immediately and inform the scheme agent (insurer) within 48 hours. This is known as a notifiable incident.

Other incidents involving injury or illness, which are not notifiable, but where workers compensation may become payable, must be notified to the scheme agent or insurer within 48 hours of the injury.

Employers are also required to keep a register of injuries that is readily accessible in the workplace. This register is a record of any injuries suffered by workers, whether they result in any claims or not. This register must be kept in written or electronic form and must be accessible to all employees.

The employer must also provide the worker with:

- First aid

- Transport to medical treatment

- The name of the employer’s insurer

- The company name and contact details of the employer

- A Workers Compensation Claims form if requested

The Personal Injury Commission (PIC) resolves workers compensation disputes between injured workers and employers.

The PIC is an independent statutory tribunal implemented by the NSW Government to deal with work and MVA injury cases.

The PIC is a dispute resolution system and its objectives are to provide a transparent, independent forum for the fair, just, timely and cost effective resolution of workers compensation disputes in New South Wales.

The Commission deals with disputes between injured workers and their employer/workers compensation insurer in relation to the benefits provided to injured workers under the Workers Compensation Act 1987. Disputes may arise about the following:

- Payment of medical and hospital expenses

- Liability for permanent impairment compensation

- How much permanent impairment compensation should be paid

- The provision of suitable duties following a work injury

- Compensation for domestic assistance

- Compensation for damage to personal property

- Compensation for the death of a worker

If you get injured at work, you must notify your employer as soon as possible of any injury and record it in the register of injuries.

- Where weekly payments are being claimed you must supply a Medical Certificate of Capacity from a registered medical practitioner and;

- Permit your medical practitioner to release information to the insurer and participate and cooperate in any injury management plan and return to work plan

All injuries sustained in the course of employment must be reported as soon as possible. Failure to report an injury within 6 months from the accident will prevent you from being able to claim unless there is a reasonable excuse.

Failure to report an injury within 3 years prevents you from claiming unless the injury resulted in the death or serious injury of the worker.

The employer of an injured worker must support the return to work of the employee. Employers are encouraged to let their employees recover while at work. This includes the development of a return to work program, with the assistance of the insurer, the general practitioner, and the injured worker.

The employer must provide suitable duties as outlined in the Workers Certificate of Capacity that includes:

- Reviewing the physical demands of the job tasks;

- Complying with the workers modified hours as outlined in the certificate of capacity

The employer should provide workplace modification and or equipment, if necessary, to allow the worker to perform the task in safety so they can recover and get back to work.

Provisional Liability enables the insurer to commence payments of weekly benefits and medical expenses to an injured worker without admitting or incurring liability under the legislation.

Provisional liability payments include the following:

- Payment of weekly compensation for a maximum of 12 weeks

- Payment of medical expenses up to $7,500

Accepting provisional liability allows the insurer more time to make a final decision on liability and whether or not to accept the Claim.

Provisional liability payments must be made within 7 days unless the insurer provides in writing a ‘reasonable excuse’ notice not to commence provisional liability payments.

Where an injury has been notified to the insurer, and there is insufficient information to determine the claim, or there has been a significant delay between the injury and the notice of injury, the insurer will have a ‘reasonable excuse’ not to commence provisional liability payments. A ‘reasonable excuse’ may include the following:

- Insufficient medical information

- The injured person is unlikely to be an employee

- The insurer is unable to contact the worker

- The worker refuses to release information about the injury

- The injury is not work-related

- The injury is notified two months after occurring

- The injury is not significant

If a reasonable excuse notice is provided, the insurer has a further 21 days to decide as to whether they will accept or decline the claim once you have provided formal notice of the claim by completing a claim form.

The Workers Compensation requires all employers to have Workers Compensation Insurance.

If, however, your employer has failed to obtain Workers Compensation Insurance, then a claim is made directly against SIRA, and they will pay the standard benefits and entitlements under the Act.

There is no difference in the procedure for claiming a psychological injury or a physical injury.

You need to from your general practitioner a Certificate of Capacity and the injury must be described as a psychological or psychiatric disorder.

That means that you must have a medically accepted psychological injury. Words such as ‘stress’ are not a psychological injury and cannot be used in claiming compensation. You must have an injury such as PTSD, depression, or anxiety or any recognisable psychological or psychiatric disorder.

You should ensure that your general practitioner has completed the certificate correctly before providing it to the insurer.

Otherwise, see FAQ How do I make a Workers compensation claim?

The insurer has a significant role in the Workers Compensation System.

When notified of an injury, the insurer must:

- Speak to the worker and the employer and consult with all relevant parties including the treating doctor to ensure the worker receives assistance to return to work

- Provide the worker with all the information necessary regarding the claims process

- Decide within 7 days whether to make Provision Liability payments or ‘reasonably excuse’ the claim

- Decide to approve and pay for medical expenses

- Decide whether the insurer or the employer will pay the worker the weekly benefits

- Develop and maintain an injury management plan for the workers to return to work

- Provide the worker with contact details of the IRO which is a body set up to assist workers in assisting with the scheme agent or insurers

- If a claim is declined the insurer must provide a written explanation outlining the reasons for denying the claim, including attaching all relevant reports and documents the insurer relied upon to decline the claim

If the insurer accepts liability for your claim, then you will receive benefits under the Workers Compensation Act.

The significant benefits include:

- Payment of weekly compensation

- Payment of lump-sum compensation for permanent impairment

- Medical and Hospital expenses

Other benefits payable are;

- Rehabilitation expenses

- Death benefits and funeral expenses

- Compensation for damage to property (e.g., clothing)

The following table outlines the weekly payments that are payable and for what period under the Workers Compensation Act.

SUMMARY TABLE OF COMPENSATION PAYABLE BY PERIOD

An injured worker is eligible for payment of the following benefits:

- Medical treatment

- Hospital treatment

- Ambulance costs

- Workplace rehabilitation services

- Travel expenses to attend Medical and Hospital rehabilitation appointments

The insurer will only pay approved expenses after they are requested to pay. If you incur medical costs without prior approval, the insurer will not pay (except for expenses incurred immediately following an injury).

The insurer will only approve payment if the treatment expenses are reasonable and necessary.

The following benefits are payable when a worker dies in a workplace accident.

- A substantial lump-sum payment for the benefits of all dependents, this increses yearly but is over $900,000

- Weekly payments for dependants

- Payments for reasonable funeral expenses.

An injured worker may obtain compensation for property damage in respect of the following;

- Artificial aids which include false teeth, artificial limbs, and spectacles

- Damage to clothing to a maximum of $600.00.

An injured worker may obtain a lump sum amount of compensation if they have sustained a permanent impairment as a result of the injury which occurred in the course of employment.

A permanent impairment is an injury that has stabilised and has resulted in an impairment that is unlikely to change within the next 12 months.

To determine if you are entitled to a lump sum amount of compensation for permanent impairment, you are assessed by an independent medical examiner known as an AMS. The AMS assesses the whole person impairment using guidelines established by SIRA.

You must obtain an assessment of greater than 10% whole person impairment to be eligible to obtain lump-sum compensation for permanent impairment for physical injuries and 15% for psychological injuries.

If you are eligible for lump-sum compensation for permanent impairment, this is payable in addition to any benefits you are entitled to receive for weekly payments and medical expenses.

The whole person impairment assessment is crucial because it will determine how long you are eligible to obtain weekly compensation and medical benefits.

You also need at least 15% WPI to make claim for damages against your employer, know as a Work Injury Damages claim.

No.

Obtaining lump sum compensation for permanent impairment is separate from your entitlement to receive benefits for weekly compensation or medical expenses.

You are entitled to receive the lump sum compensation for permanent impairment and continue to receive weekly benefits and medical expenses if you are eligible.

Yes.

Weekly payments may be suspended, reduced, or stopped by the insurer as a result of the following:

i. Failure to provide documents

If you fail to provide a Medical Certificate of Capacity, then the insurer will stop making weekly payments of compensation.

ii. Comply with the return to work obligations

If you fail to comply with reasonable request to return to suitable employment, weekly payments may be suspended

iii. The insurer issues a work capacity decision

The insurer can stop or reduce weekly payments if they disagree with your certificate of capacity and believe you have a greater capacity for work.

iv. The insurer declines liability for the claim

The insurer can stop payments if they believe your injury is no longer work-related.

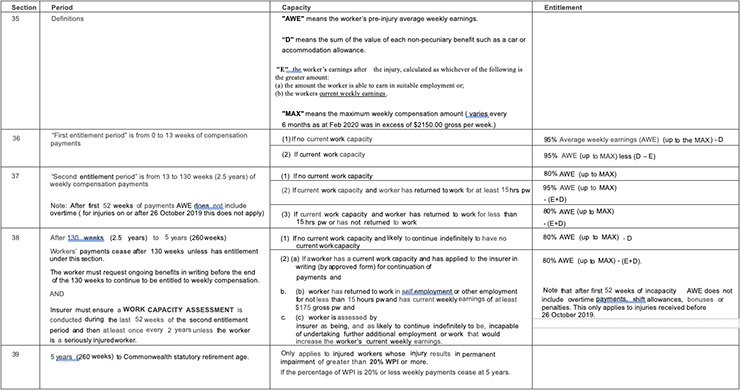

v. After 130 weeks of weekly payments

A worker has no entitlement to weekly payments of compensation after 130 weeks unless:

(a) The insurer has assessed that the worker has no capacity for employment; or

(b) The worker has the capacity for work and has applied to the insurer for a continuation of weekly payments; and

(c) The worker is working 15 hours or more per week; and

(d) The worker is earning at least $173.00 per week; and

(e) The worker has been assessed by the insurer as incapable of undertaking further employment to increase their earnings.

If you can work and are not working at least 15 hours per week (and earning at least $173.00 per week), weekly payments will be stopped.

vi. After 260 weeks (5 years) of weekly payments:

Weekly payments will stop for all workers after 5 years unless you have greater than 20% whole person impairment.

If your impairment is greater than 20%, then payments will continue if:

- You are unable to work; or

- You have some capacity for work and are working at least 15 hours or earning more per week and earning at least $173.00 per week

vii. Your entitlement ceases under the Workers Compensation Act due to your age.

Weekly payments of compensation will also cease on the anniversary of your statutory retirement age, usually age 68.

In each of these circumstances, the insurer must notify you in writing, giving the reasons why your payments have been stopped, reduced or suspended. They must provide you with all reports or other documents they rely upon in stopping, reducing, or suspending the payments of weekly compensation.

If this happens to you, please contact us immediately.

The insurer can decline or stop payment for medical treatment for the following reasons:

i. They do not believe that the treatment is because of the injury sustained; or

ii. They do not think the treatment is reasonable and necessary or

iii. Your entitlement to payment of medical expenses ceases in accordance with the Workers Compensation Act.

The insurer can, at any time, decline to approve payment of medical treatment if they do not believe it is related to your injury or if they do not think it is reasonable and necessary. They must do so in writing, setting out the reasons for declining to pay. This is called a Section 78 Notice.

If this happens to you, please contact us immediately.

Medical expenses are required to be paid by the insurer as follows;

- If no weekly payments are made, then medical expenses are paid for up to 2 years after the date of the injury or;

- If weekly payments are paid up to 2 years after the last date on which you received weekly compensation benefits.

If, after medical expenses cease, you have a further period where you are not fit to work, and weekly payments are recommenced, the insurer will again become responsible for payment of medical expenses, and approval should be sought directly from the insurer.

The 2 years can be extended to up to 5 years if your WPI is greater than 10% and less than 20%.

If your WPI is assessed as 21% or more then medical expenses are payable for life.

Suitable employment, as defined in the Act as appropriate employment that considers:

- The nature of the workers injury and incapacity

- The workers age, education, skill and work experience

- Any return to work plan

- Any rehabilitation services provided

And does not have regard to:

- Whether the work or employment is available

- Whether the work or employment is the type or nature that is generally available in the employment market

- The nature of the worker’s pre-injury employment

- The worker’s place of residence

This is a very wide definition of suitable employment. It essentially means that suitable employment could be work, such as a car park attendant, receptionist, or very light office type work.

Should the insurer find, a worker is physically capable of undertaking such work, then it will be regarded as suitable employment regardless of whether any such positions are currently available.

Insurers can reduce or terminate weekly compensation by making a Work Capacity Decision. If you disagree with such a decision, you will need the assistance of a lawyer.

An employer of an injured worker has obligations under the Act to assist the worker in returning to suitable work as soon as possible following an injury.

They must assist in the development of a return to work program and offer suitable work to support the recovery of the worker.

If an employer does not have suitable duties, then the employer is not obligated to provide such work. Suitable duties are duties that can be provided, which are in line with the worker’s capacity for work and which are meaningful and give some purpose for the employer.

If the employer has no such suitable duties and you are certified fit for suitable work, then you must seek those suitable duties with an alternate employer, either yourself or through the assistance of a rehabilitation provider. You have an ongoing obligation to look for suitable work even if your employer cannot provide you with such work.

The insurer will typically appoint a workplace rehabilitation provider to assist you and the employer with your return to work. The primary goal is that you return to work in the position you held at the time of your injury. If this is not achievable due to the nature of the injury you sustained, then the next goal is to return the worker to the same employer in some suitable or light work. If this is not possible, then the goal of the rehabilitation provider is to assist you in providing suitable work with a different employer.

Often large employers nominate an employee (or a contractor) to assist injured workers in returning to work. They ensure that the employer and the employee are doing their best to comply with their rights and responsibilities under the Act in returning the worker to suitable employment.

The scheme agent or insurer will usually appoint an approved workplace rehabilitation provider to help injured workers to return to work. The workplace rehabilitation providers responsibilities are to:

- Identify and design suitable duties for the worker to assist the employer in meeting their obligations to provide suitable employment

- Identify and co-ordinate strategies to return the worker to perform their duties

- Promote early return to work

- Act as a link between the insurer, employer and treatment providers

- Arrange appropriate re-training and place in any alternative employment where the worker can return to preinjury duties

- Assist the worker to return to work

You can choose the Rehabilitation provider; you do not need to accept the one appointed to you by the insurer.

Yes. An insurer can dispute any part of or your entire claim.

When disputing your claim, the insurer under Section 78 of the Workers Compensation Act must provide you a written notice of the reasons why the claim is declined and give a copy of all medical evidence and other documents that they rely upon in rejecting your claim.

A claim can be declined for the following reasons:

- The insurer does not believe you got injured at work

- The insurer does not believe the injury is any longer work-related

- The insurer believes you have recovered from your injury and can return to work

- The insurer does not accept the medical treatment you have requested as reasonable or necessary

- The insurer has medical evidence which states that your injury is not work-related

The insurer cannot stop payments of weekly compensation until they have provided you with written notice of the reasons why the claim is declined and a period of notice.

If this happens to you, you should contact us immediately as you can challenge this decision in the Personal Injury Commission of NSW.

If you receive a Section 78 Notice declining liability for your claim, then you should contact your lawyer immediately and provide them with a copy of the notice.

You are also entitled to request a review of the decision to decline your claim from the insurer; however, your lawyer will assist you in preparing this review.

In our experience, a review of the decision to decline liability for the claim by the insurer is rarely overturned, and you need to challenge the decision to decline your claim in the Personal Injury Commission of NSW.

Disputes about suitable employment and suitable duties may arise where the employer does not offer appropriate suitable tasks or where the insurer and your doctor disagree as to the type and nature of suitable duties.

Disputes about suitable employment are Injury Management Disputes. They can be referred to the Personal Injury Commission for determination.

If you have any aspect of your claim for workers compensation declined by an S.78 Notice, your lawyer will make an application to the Personal Injury Commission (PIC) to appoint an independent Member to hear and determine the issues in dispute.

The process is as follows;

- Your lawyer files an Application for Dispute resolution with the PIC, which includes all evidence used in making the decision.

- The Insurer or its lawyer must file a reply with their evidence within 28 days.

- The matter is reviewed by the PIC, and a telephone conference is usually appointed 28 days later.

- The PIC notifies you of the date and time of the telephone conference.

- You should attend the telephone conference in person via the telephone.

- At the telephone conference, the Member will discuss the matter and the issues in dispute. The Member will attempt to resolve the matter by agreement. If not, the Member will make orders for further preparation of the claim and list the matter for a face to face Conciliation/Arbitration Conference. Your lawyer will do the majority of the talking at the telephone conference.

- Your lawyer will then confirm in writing the date and time of the Conciliation/Arbitration Conference, which is usually 28 days following the telephone conference.

- If further preparation is necessary, your lawyer will contact you for details.

- The Conciliation/Arbitration Conference has two phases;

- The Conciliation phase – the Member, will discuss the issues and see if the parties can reach agreement if no agreement can be reached the matter proceeds to;

- The Arbitration phase – the lawyers are asked to make submissions outlining what the outcome of the claim should be, and occasionally questions are requested by the Member about the claim. The Member then makes a written decision within 21 days.

- The members decision is final and binding on both you and the insurer unless the Member has made an error of law.

- The outcome is confirmed by the PIC 28 days later.

- The insurer will then pay the compensation awarded to you.

- Usually, 10% of that lump sum is deducted and sent to Medicare as a deposit until it is determined if Medicare is owed any money.

If you have been unable to reach an agreement with the insurer on the percentage of whole person impairment (WPI), your lawyer will make an application to the Personal Injury Commission (PIC) to appoint an independent medical specialist to assess the percentage WPI.

The process is as follows;

- Your lawyer lodges an Application for Dispute resolution with the PIC, which includes all evidence considered.

- The Insurer or its lawyer must lodge a reply with their evidence within 28 days.

- The PIC reviews the matter; if the only issue is the percentage WPI, the PIC arranges a medical examination for you to attend with an Approved Medical Specialist (AMS).

- You are notified of this appointment approximately 28 days after the reply is lodged.

- We will notify you of the details of the medical appointment which you must attend.

- The AMS, usually within 28 days, after the appointment, will write a report to the PIC. The PIC will review the report and ensure there are no errors.

- The report is sent to your lawyer.

- Your lawyer will send you a copy of the report and discuss the outcome.

- An AMS assessment is usually final and binding on both parties unless there has been some error by the AMS. Either the insurer or you can Appeal if an error has occurred.

- Usually, the outcome is simply confirmed by the PIC 28 days later.

- The insurer will then pay the compensation awarded approximately 6 – 8 weeks later, which we will send to you.

- Usually, 10% is also deducted from the lump sum and sent to Medicare as a deposit until it is determined if Medicare is owed any money.

- Sometimes the PIC, instead of arranging an AMS appointment, will list the matter for a telephone conference to discuss any issues raised by the insurer.

Once an Application to Resolve a Dispute is lodged with the Personal Injury Commission, the insurer has 28 days to lodge a reply. Once the Reply is received, the PIC will appoint a date and time for a telephone conference.

The telephone conference will take place via the telephone.

The telephone conference is between the injured person, their lawyer, the insurance company representative or their lawyer and an independent Member appointed by the Personal Injury Commission.

Your Lawyer will do most, if not all of the talking during the telephone conference.

You are however required to attend either in person (preferable) or on the telephone.

At the telephone conference the Member will discuss the following:

- The likelihood of settlement

- That all parties understand the process

- Whether the parties can agree on any of the issues in the proceedings

- Any legal or other issue that must be determined before the matter can proceed further

- Whether the matter is to be listed for an Arbitration date or referred to an independent doctor for assessment

If the matter is unable to be resolved at the telephone conference and the matter is ready to proceed, the Member will arrange a Conciliation Conference/Arbitration Hearing. This usually occurs approximately 1 to 2 months following the telephone conference.

If an agreement is reached at the telephone conference then the matter is finalised by signing the paperwork to record the agreement.

The telephone conference usually takes between 15 to 45 minutes

Once an Application to Resolve a Dispute is lodged with the Personal Injury Commission (PIC), the insurer has 28 days to submit a reply. Once the Reply is received, the PIC will appoint a date and time for a telephone conference.

The telephone conference will take place on the phone.

The telephone conference is between the injured person, their lawyer, the insurance company representative, or their lawyer and an independent Member appointed by PIC.

Your lawyer will do most, if not all, of the talking during the telephone conference.

You are, however, required to attend on the telephone.

At the telephone conference the Member will discuss the following:

- The likelihood of settlement

- That all parties understand the process

- Whether the parties can agree on any of the issues in the proceedings

- Any legal or other issues that must be determined before the matter can proceed further

- Whether the matter is to be listed for an Arbitration date or referred to an independent doctor for assessment

If the matter is unable to be resolved at the telephone conference and the matter is ready to proceed, the Member will arrange a Conciliation Conference/Arbitration Hearing. This usually occurs approximately 1 to 2 months following the telephone conference.

If an agreement is reached at the telephone conference, then the matter is finalised by signing the paperwork to record the agreement.

The telephone conference usually takes between 15 to 45 minutes.

Disputes regarding the degree of permanent impairment or whether medical expenses are reasonable and necessary will be referred directly to an Approval Medical Specialist by the Personal Injury Commission (PIC).

An Approved Medical Specialist (AMS) is a doctor who is a medical specialist with suitable experience and training by SIRA. They are to provide an independent and unbiased assessment of the injuries. There is a panel of doctors that the Personal Injury Commission used for these examinations, and one will be appointed to determine your claim for permanent impairment or medical expenses.

The Approved Medical Specialist is not appointed by the workers compensation insurer or by your lawyer; they are appointed independently.

The PIC arranges the medical examination and will let your lawyer know the date and time of the assessment and the name of the approved medical specialist. The examination will take place at the doctor’s practice, and a report will then be provided directly to the PIC, usually within 21 days. The report is checked for errors by the Commission, and if satisfied that it is correct, the report is provided to your lawyer.

The report will outline your level of whole person impairment, and the reasons for deciding the percentage WPI following the Medical Assessment Guidelines and or will outline whether medical treatment is reasonable and necessary.

Can I appeal the decision of the approved medical specialist?

Yes, an appeal can be made against the approved medical specialist but must be made within 28 days of receipt of the medical assessment. You can only appeal on the following basis: –

- The medical assessment was made based on some incorrect criteria

- The medical assessment contained a demonstrable error

- Your condition has deteriorated, and there is an increase in permanent impairment since your last examination.

- You have additional relevant information that was not available to the approved medical specialist; or

- A combination of the above.

Once an appeal is lodged with the PIC, the matter is referred to an appeal panel consisting of 2 approved medical specialists and one legal Member. The medical appeal panel reviews the documents and decides whether the matter can be: –

- Determined on the papers

- Whether new evidence should be allowed

- Whether a further medical examination should take place

The Appeal Panel then makes a new decision which can confirm the prior determination or make any change they think is necessary.

You will be asked to attend medical examinations by your lawyer and the insurance company.

The purpose of the medical examination is for a suitably qualified doctor to provide an opinion concerning your injury in respect of the following:

- What injury or medical condition you have as a result of the injury.

- The cause of that injury or medical condition.

- If an accident or the nature of your work has aggravated an underlying condition.

- The prognosis for your injury is, what is likely to happen in the furture?

- Your ability to work as a result of the injury.

- An assessment of the percentage of whole person impairment.

The examination is intended to be independent, honest, and impartial, as possible.

The examination can be arranged by usually one of the three parties to a legal case as follows:

- Your solicitor

- The insurance company or its solicitor

- An independent body such as the Workers Compensation Commission or the Motor Accidents Authority

Before attending a doctor, you should make sure you know who has arranged the examination, and if you are unsure, you should ask your lawyer.

Once the examination is complete, a report will be sent by the doctor who examined you to the person who has arranged the examination. That person will usually pay for the cost of the doctor’s report. The report is confidential. The report recipient does not need to provide a copy of the report to anyone else or even you.

The doctor you will see is usually a specialist in the area most relevant to the injury you have sustained, such as an Orthopedic Specialist for a knee or back injury. The doctor is also usually a consultant, which means they have generally retired from private practice. Typically, the doctor only prepares medico-legal reports and no longer treats any patients.

You are not seeing the doctor like his/her patient; the doctor is not able to give you advice about your medical problems. The doctor also cannot give you any treatment. Any advice about your condition or treatment should be obtained from your medical practitioners and not from a medico-legal doctor.

You should ensure you have the correct appointment date, time, and address. A failure to attend an appointment usually results in a cancellation fee of a few hundred dollars, which you will be required to pay.

If you need an interpreter, you should request one to be available.

You need to take with you all x-rays, scans, and all other tests that you have had relevant to your condition so the doctor can make a complete assessment.

The doctor will introduce himself and, by agreement, may allow you to have a friend or relative with you during the examination. That person should not interrupt or interfere with the examination.

The doctor will ask questions regarding the accident and the circumstances that caused it. He or she will ask you about your treatment and how the injury affects you now. He or she may ask you about your past medical history, employment history, and lifestyle.

The doctor will carry out a physical examination, both in respect of the injured parts of your body but also to other body parts as well.

If the doctor asks you to do something that will cause pain, then please mention this to the doctor. You are supposed to co-operate with the doctor; however, you do not need to be in pain.

If the doctor asks you a question that you do not wish to answer, then you may say so. If the doctor wants to examine you and you do not agree, you may also refuse. Any refusal, however, will be mentioned in the medical report.

The doctor should carry out the examination in a respectful manner and not hurt you.

Usually, a medico-legal examination takes between 30 minutes to 1 hour. Some even shorter, depending on what the doctor is assessing.

The doctor will ask you questions which they consider relevant and will aim to let you go as soon as possible.

If you cancel an appointment within 24 hours, usually the Doctor will charge a non-attendance fee for which you may be responsible for payment.

Work capacity was introduced in the NSW workers compensation system in October 2012.

It is an assessment of an injured worker’s ability to return to pre-injury employment or some other suitable employment. The insurer conducts an assessment, and that assessment is used to make a work capacity decision.

A work capacity decision is a decision made by the insurer about an injured workers current capacity for work.

A work capacity decision is a decision made by the insurer about the following matters: –

- A worker’s current capacity for work.

- What suitable employment can a worker undertake?

- What amount is an injured worker able to earn in suitable employment?

- What is the amount of the workers pre-injury weekly earnings?

- Any decision which affects the workers entitlement to weekly payments of compensation.

A work capacity decision can be made at any point throughout the life of the claim but is usually undertaken shortly before the worker has received 130 weeks of weekly compensation.

The work capacity decision will determine whether any weekly payments of compensation are payable under the Act and, if so, the amount of compensation that is payable.

A work capacity decision must be appealed/reviewed as follows: –

- Firstly, request an internal review by the insurer by completing a work capacity application for internal review by the insurer.

- If you are not satisfied with the outcome of the insurer’s internal review then before the decision taking effect you need to lodge an Application for Dispute Resolution with the Personal Injury commission of NSW

Your lawyer will assist you in making this application.

A claim for Work Injury Damages must be submitted within three years from the date of your injury. If you do not bring a claim within three years, you need to obtain leave to proceed out of time from the District Court of NSW. Such consent can be obtained if there is a satisfactory reason for the delay. However, if leave is declined, you can be prevented from proceeding with a claim at all. It is, therefore, crucial to ensure that any claim for work injury damages is commenced within three years from the date of your accident.

Yes. You can sue an employer for injuries sustained under the Workers Compensation Act if you can establish the following:

- That you have an assessment of whole person impairment of 15% or greater and;

- That you sustained your injury as a result of your employer’s failure to take reasonable care while in the course of your employment.

If you injury was caused by your employer failure to take care, you may have an entitlement to seek payment of lump sum compensation for damages modified by the Workers Compensation Act.

The Workers Compensation Act allows only for payment of compensation or damages in respect of past and future loss of income.

You are not entitled to claim damages for pain and suffering, future medical treatment, or future care and assistance in a claim against an employer.

These restrictions only apply to a claim for negligence against an employer. They and do not apply in a claim against a non-employer.

A common example of this is on a building site. A worker may get injured as a result of scaffolding collapsing, which was not the fault of the employer ( a plastering company) but it was the fault of the person who erected the scaffolding. You can sue the person or company responsible for erecting the scaffolding.

Motor Accidents Frequently Asked Questions

To claim compensation, you must have sustained an injury due to the use or operation of a boat in NSW.

Any kind of user can claim the Act, including; the driver or the passengers.

The system is no longer fault-based; anyone injured by a boat can claim statutory benefits no matter who caused the accident.

To make a claim, you need to do the following –

- Seek immediate medical assistance from your local general practitioner or, if necessary, the emergency department of the nearest hospital.

- Report the accident to the police within 28 days and obtain an event number.

- If you can, get the following information: –

a. The name, address, licence details, and phone number of any driver of the vehicle involved in the accident.

b. The make, model, and number plate of any boats involved in the accident.

c. Contact details of any witnesses.

d. If possible, take photographs of the accident scene, including the location and damage to any boats.

If the injury is a result of a boat accident that is also work-related, you will also need to make a worker’s compensation claim against your employer’s worker’s compensation insurer.

To claim compensation, you must have sustained an injury due to the use or operation of a motor vehicle in NSW.

Any kind of road user can claim the Act, including; the driver, the passenger, pedestrian, cyclist, or motorcyclist.

For the first 52 weeks of benefits the system is no longer fault-based; anyone injured by a motor vehicle can claim statutory benefits no matter who caused the accident.

To make a claim, you need to do the following –

- Seek immediate medical assistance from your local general practitioner or, if necessary, the emergency department of the nearest hospital.

- Report the accident to the police within 28 days and obtain an event number.

- If you can, get the following information: –

a. The name, address, licence details, and phone number of any driver of the vehicle involved in the accident.

b. The make, model, and number plate of any cars involved in the accident.

c. Contact details of any witnesses.

d. If possible, take photographs of the accident scene, including the location and damage to any vehicles.

You then need to make an Application for Personal Injury Benefits through the SIRA website HERE.

If the injury is a result of a motor accident that is also work-related, you will need to make a worker’s compensation claim against your employer’s worker’s compensation insurer rather than a CTP claim.

You cannot claim if you are charged with a “serious driving offence” in connection with the accident or were the at-fault driver of an uninsured vehicle.

The accident must be ‘verified’ before a claim can proceed – there must be proof that the accident happened. The best evidence is reporting the incident to the police within 28 days.

The police will give you an event number, which you must include in the Application form.

Verification of accidents will prevent people from making exaggerated or false claims and ensure that the scheme supports people in genuine need.

The simplest form of verification is a police event number, so you should report the accident to the police as soon as possible if they did not attend the scene. You can do so by contacting the Police Assistance line on 131 444.

Other forms of evidence could include news reports, photos of the accident scene, or statements from witnesses.

If you are unable to identify the registration number of the vehicle which caused the accident or if the vehicle was not registered, you can claim against the Nominal Defendant.

You still need to make an Application for Personal Injury Benefit through the SIRA website.

You must have tried everything possible to find out the registration number of the vehicle, including speaking the police, talking to witnesses, or by putting an advertisement in the newspaper or flyers in local letterboxes. You must do what you can to find out if anyone can identify and provide you with the registration number of the vehicle.

If you have been unable to identify the vehicle which caused the accident, then you can lodge a claim form with the Nominal Defendant.

To make a claim, you must complete an Application for Personal Injury Benefits through the SIRA Website HERE.

You will need the registration number of the vehicle you consider most at fault.

You must have notified the Police of the accident within n28 days and have an event number.

If you don’t know the registration number (license plate), you might be able to get it from the police. Look at your police report, or contact the Police Assistance Line on 131 444.

You need to take all reasonable steps to find the registration number, but if you can’t, you can still make a claim. Call CTP Assist on 1300 656 919 for assistance.

If you believe you were at fault, you can still make a claim. You will provide the registration number of the vehicle you were driving.

Anyone injured in a motor vehicle accident in NSW regardless of who was at fault can receive up to 52 weeks of income support and medical expenses by completing an Application for Personal Injury benefits through the SIRA website HERE.

This includes:

- drivers and passengers

- riders and pillion passengers

- pedestrians

- cyclists.

The Application entitles you to claim statutory benefits for loss of income and medical expenses incurred for up to 12 months.

Once an application is made the following will occur –

- Contact You: The insurer will contact you within three days after you lodge a claim. They will confirm they have received your application and will outline the next steps in the process. They should also provide a claim number and their contact details. If you need immediate medical treatment, ask the insurer to explain what you should do next (including how you can be reimbursed for your medical expenses so far).

- Investigate: The insurer will investigate your claim, including reviewing the police report and other evidence such as medical reports from your treating doctor/health professional. The insurer may ask you to see other medical specialists.

- Make a decision: The insurer must tell you within four weeks if they’re accepting or denying the claim. If the insurer denies liability, they need to give a full explanation of their reasons. This must include the consequences of their decision (including the effects on your entitlements and when it will take effect), copies of the information they used in making the decisions, how you can seek a review the decision, and where to go for further help in understanding what to do next.

- Payments: The insurer will start making payments to you within 14 days if they accept your claim. Most people will also need to start a recovery plan. A recovery plan is designed to return you to full pre-accident activities as soon as possible. It is prepared in consultation with you, your doctor, and any relevant treating practitioners.

The insurer will pay the following benefits once the claim is accepted.

- Income support –

If you get injured in a motor accident, and as a result, you have a loss of earnings, you may be entitled to income support payments.

Regular income support payments compensate you for some of the income you have lost because of your injury. If you’re off work, these payments will help pay the bills, so you can focus on getting better.

These payments will be a percentage of your pre-accident earnings:

- for the first 13 weeks, the maximum is 95 percent

- after 14 weeks the maximum is 85 percent (depending on whether you have total or partial loss of earning capacity)

- Medical expenses –

The insurer may pay for all reasonable and necessary expenses for injury resulting from the accident. This includes:

- medical, dental and pharmaceutical expenses

- rehabilitation and treatment expenses (like physiotherapy)

- the cost of traveling to and from appointments

- in some cases, support services (like personal care and help around the home).

Once you have completed the Application for Personal Injury Benefits and the claim is accepted, the insurer will pay loss of income and medical expenses for up to 52 weeks.

This can be extended for up to a maximum of three years for income support and life for medical expenses if;

- You were not wholly or mostly at fault and;

- You have a “non threshold injury.”

The insurer is required to decide these two matters within about 9 months from the date of injury.

This is a significant decision as it affects your ability to obtain proper compensation for your injuries.

You should always seek advice from a lawyer about this decision as you may be entitled to thousands of dollars in compensation.

If you disagree with this decision, it can be challenged by your lawyer; however, there are strict time periods in which to make such a challenge.

Yes, but only if the insurer decides that;

- You were not wholly or mostly at fault and;

- You have more a “non-threshold injury.”

The insurer is required to make this decision in writing and send it to you within 12 months of the accident, this usually happens around 9 months after the accident.

If the insurer accepts both matters, then payments can be extended as follows;

- Income Support for up to three years (as long as you make a claim for common law damages) and;

- Medical expenses and care for life.

You should also see a lawyer and make a common law claim for damages, this is a claim for lump sum compensation for pain and suffering and future loss of income and loss of superannuation.

This common law claim must be made within 3 years from the date of the accident.

No compensation is payable after 52 weeks if the insurer considers you were “wholly or mostly” responsible for the accident. That is, who caused the accident?

The insurer will investigate the circumstances by obtaining the Police report and often requesting an investigator to obtain statements from everyone involved in the accident, including you, the injured person and the drivers. You need to be careful when giving your statement to the investigator as the insurer may use this against you.

You can still claim even if you were partly at fault. This is known as contributory negligence. The contributory negligence of the injured person involved must not be greater than 61%. The insurer will decide who was at fault and if necessary determine what percentage applies to the injured person. If you are assessed at 62% or more responsible for the accident then you are “wholly and/or mostly at fault” and will not be able to claim after 52 weeks of benefits.

If you disagree with this decision, you should contact us immediately; you only have 28 days to seek a review of this decision.

The Motor Accidents Injuries Act 2017 defines a threshold injury as follows: –

- Soft tissue injury.

- A minor psychological or psychiatric injury.

A soft tissue injury is:-

“an injury to the tissues that connects supports or surrounds other structures or organs of the body (such as muscles, tendons, ligaments, menisci, cartilage, fascia, fibrosis tissues, fat, blood vessels and synovial membranes) but not an injury to nerves or a complete or partial rupture of tendons, ligaments, menisci or cartilage.”

The regulations add the following: –

“an injury to a spinal nerve root that manifests in neurological signs (other than radiculopathy) is included as a soft tissue injury.”

A minor psychological or psychiatric injury:-

“a psychological or psychiatric injury that is not a recognised psychiatric illness.”

If you have sustained PTSD or depression as a result of a motor vehicle accident, this is a recognised psychiatric injury and therefore is not a minor injury.

If you disagree with the decision made by the insurer about whether you have a threshold injury, you can refer the matter to the Personal Injury Commission to resolve this dispute. The PIC will appoint an independent assessor to make a binding decision.

You should seek the assistance of a lawyer as the law is complex and strict time limits that apply.

There have now been several decisions made by the PIC concerning what constitutes a “threshold injury” and here are some examples: –

Example 1

The claimant was a front-seat passenger in a vehicle at the traffic lights, which was rear-ended by another car. The claimant reported a brief loss of consciousness, was taken to hospital by ambulance. The claimant subsequently consulted a general practitioner and had pain in the right side of the neck, low back, right leg, and right knee. The claimant underwent 18 sessions of physiotherapy and continued to consult his general practitioner.

On examination, the claimant had a reduced range of motion in the neck but no muscle spasm or guarding, a reduced range of motion in the lumbar spine, but with no muscle spasm or guarding and no neurological symptoms.

The claimant was diagnosed as suffering soft tissue injury to the cervical spine, right shoulder, low back, left chest, and right knee. There was no radiculopathy present. The claimant had a minor injury as it satisfied the definition of minor injury in that all injuries sustained were soft tissue, and there were no neurological signs such as radiculopathy present.

The claimant was, therefore, only entitled to weekly payments and medical expenses for a period of 12 months.

Example 2

The claimant was again involved in a rear-end motor vehicle accident reporting immediate neck pain with radiation of pain across both shoulders and into the upper back. The DRS assessor found that the claimant had sustained a whiplash injury to the cervical and upper thoracic spine with referred symptoms into the left and right shoulder region. There was no evidence of radiculopathy or any neurological condition. There was no injury involving any torn ligaments, tendons, or nerves.

This was considered a minor injury as it was soft tissue only.

From a physical perspective to have more than a threshold injury, there needs to an injury involving torn ligaments, tendons, or nerve damage such as radiculopathy. Bodily disfigurements, any eye injury, hearing loss, organ damage, or fracture/broken bone will be enough to qualify as more than a minor injury.

However, any spine injury that does not produce radiculopathy that is, nerve damage, does not and will be considered a threshold injury. Such spinal injuries are considered “soft tissue.”

The definition is harsh, and people with serious injuries will often not qualify for benefits after 52 weeks or be able to make a Common Law claim as they will are classified as having a threshold injury.

Example 3

The following example of psychological injuries is helpful;

A claim involved a claimant who was driving with his family. As the claimant slowed down and indicated to turn left, a vehicle collided with the rear of their car. The claimant lost control of the vehicle and spun around to face another vehicle, which collided with the claimant’s car. The claimant was concerned with the welfare of his family members and was subsequently transported to a hospital with soft tissue injury.

The claimant subsequently consulted his general practitioner with complaints of a stiff neck, pain, headaches, and insomnia. The claimant was referred to a physiotherapist and treated with analgesic medication. The physical injuries were considered minor injuries as they were soft tissue in nature.

The claimant, however, also had a psychological condition as he was suffering from intrusive and recurrent memories of the accident, flashbacks, disturbed sleep, irritability, persistent thoughts of self-blame and guilt, fluctuating appetitive, reduced energy and lack of motivation and unable to drive due to increased anxiety.

The initial diagnoses were one of an adjustment disorder with mixed anxiety and depressed mood — subsequently, a determination of post-traumatic stress disorder was made.

An acute stress disorder or an adjustment disorder is considered to be a minor psychological or psychiatric injury.

Post-traumatic stress disorder is not considered to be a minor psychiatric injury. While the claimant’s condition had begun initially as an acute stress reaction, it had developed into post-traumatic stress disorder and therefore was not considered to be a minor psychiatric injury.

The insurer’s decision as to whether the injury is a threshold injury can be challenged through the Personal Injury Commission.

You will need the assistance of an Accredited Specialist in Personal Injury Law to assist in making this application to PIC as it may require obtaining medical evidence from your treating doctors to assist in determining whether the injury is a threshold injury.

There are many different types of disputes which can arise in a motor accident claim.

Generally, if you do not agree with the insurer’s decision, you will need to request an internal review within 28 days of receiving the decision. The insurer will provide you a form to complete. Lawyers are not paid to assist with internal reviews.

After the internal review, the insurer makes a further decision. If you still disagree, you need to make an Application to the Personal Injury Commission for an independent decision, usually this needs to be made within 28 days.

You can use the assistance of a lawyer to make an application to PIC in certain circumstances.

Disputes can arise concerning: –

- Whether the death or injury has resulted from a motor accident in the state of NSW

- Whether the motor accident concerned was caused by the fault of another person

- Whether the motor accident was caused by the injured person (contributory negligence)

- Whether the claimant has suffered threshold injuries and is not entitled to statutory benefits after 52 weeks of the date of the accident

- Whether a serious driving offence was committed (no statutory benefits)

- Whether the claimant has given full and satisfactory response for non-compliance with a duty or a delay (E.g., not making a claim within the statutory time frame or not reporting the accident to the police within the statutory time frame.

- Whether the motor accident verification requirements have been complied with.

There are many other types of disputes which can arise, and you should contact a lawyer for assistance.

If the insurer accepts your claim, then they will engage in early rehabilitation to assist you with treatment after the motor vehicle accident. Rehabilitation aims to return the injured person to a level of function and quality of life comparable to their pre-injury level. To do this, they usually appoint a rehabilitation provider. A rehabilitation provider is a company appointed by the CTP insurer to provide rehabilitation services which include Occupational Therapist, Rehabilitation Counselors, Psychologist, and Exercise Psychologists.

The rehabilitation provider’s role is to assist you in developing a plan and goals to assist in your recovery and return to work.

The rehabilitation provider will also assist the insurer in determining what treatment is reasonable and necessary.

You can claim common law damages if the insurer has accepted that the driver of the motor vehicle was at fault, and you have more than a “threshold injury.”

As part of the investigation of your claim, the insurer will obtain information about your medical condition from your treating doctors and or by arranging for you to be assessed by other medical specialists appointed by the insurance company.

They will also ask several questions called “particulars” about the injuries you have sustained, your impairments and disabilities arising from those injuries, and any economic or non-economic loss you are claiming. This information will help the insurer to make a reasonable offer of settlement to finalise your claim. Your lawyer, on your behalf, should answer these particulars.

The insurer will, once your medical condition stabilises, then make an offer of settlement.

If you receive an offer of settlement, you need to immediately seek advice from your lawyer who specialises in motor vehicle claims. You should not try and negotiate a resolution with the insurer yourself. A lawyer will almost always obtain for you significantly more compensation than you can on your own.

If you accept an offer of settlement from the insurer, then your claim is finalised. If your claim is finalised, you are not entitled to any further income support payments.

You continue however to be entitled to payment of medical expenses and care for the remainder of your life.

If you are unable to negotiate a resolution of your claim with the insurer, then you will need assistance from a lawyer to resolve your dispute through the dispute resolution process known as DRS.

The basic principle of Contributory negligence is that where the injury sustained to a person is a result partly from that person’s own fault and partly the fault of another driver, the amount of compensation payable is reduced having regard to the injured persons share in the responsibility for causing the accident.

For example, if the injured person failed to keep a proper lookout, which may have avoided the collision, then the amount of compensation could be reduced by say 25%.

Non-Economic loss is the payment of a lump sum amount of compensation for pain and suffering and loss of enjoyment of life.

The payment of a lump sum amount is only made to those who have sustained severe injuries in a motor vehicle accident.

An independent medical assessor must assess you as having greater than 10% whole person impairment to receive any compensation for non-economic loss.

You firstly try to agree with the CTP insurer that you exceed the 10% whole person impairment threshold. If you are unable to agree with the insurer, an application is made to PIC, who appoints an independent medical assessor who will review your medical records and examine you to determine your percentage of whole person impairment.

If you are assessed as having a permanent impairment greater than 10%, then you are entitled to claim non-economic loss, if your assessment is 10% or less than you are not entitled to any compensation for non-economic loss.

The percentage WPI does not determine how much compensation you receive only that you reach the threshold to be entitled to claim such compensation.

The maximum payable for a most extreme case of non-economic loss is currently ( April 2026) $691,000 ( this is increased each year). You generally receive some part of this amount having regard to the seriousness of your injuries compared to the seriousness of a most extreme case. Usually, most awards of non-economic loss are between $250,000 and $350,000 but each cases varies according to the circumstances.

Economic loss is compensation for loss as a result of losing money due to an inability to work.

You are entitled to the following types of economic loss:

- Loss of income in the past or future due to an inability to work due to your injuries

- Loss of Superannuation contributions your employer would have made both for the past and future.

To claim non-economic loss, that is, pain and suffering, you must have a whole person impairment of greater than 10%.

Usually, your lawyer will arrange for you to be assessed for whole person impairment. You will consult a Doctor who is using the guidelines to assess the % WPI.

Your lawyer will then try and reach an agreement with the insurer that you exceed 10% WPI.

If the insurer does not agree, an application will be made to the Personal Injury Commission to appoint an independent Doctor to assess the level of WPI. This is a final and binding assessment on both you and the insurer.

The assessment can be appealed if there is an error is the method of assessing the WPI.

The whole person impairment assessment is calculated by medical assessors who determine the level of whole-person permanent impairment based on the following:

- Guidelines as to how permanent impairments are made which are published by SIRA

- Examine your medical records

- Conduct a physical medical examination

Based on the guidelines, your medical records, and the physical examination, the medical assessor determines the level of whole-person permanent impairment.

Your lawyer will arrange for you to be examined by a Doctor to assess the WPI and a claim made to the insurer to see if they agree. If no agreement is reached, an Application is made to PIC to appoint an independent Doctor to assess the level of WPI.

If you have made a common law claim, your lawyer will obtain all necessary evidence to prove your entitlement to claim;

- Non-economic loss, that is, pain and suffering and;

- Loss of income and superannuation, both past and future.

Your lawyer will attempt to reach an agreement with the insurer, usually at a settlement conference, as to the amount of compensation payable as a lump sum. If an agreement can be reached, the claim resolves, payment is usually made in about 6 weeks.

If an agreement cannot be reached, your lawyer will make an Application to PIC to appoint an independent Member who will act like a Judge to hear and determine how much compensation you are entitled to receive.

Yes, the new Motor Accident Legislation for injuries received on or after 1 December 2017 now provides very strict time limits in which to make a claim.

These include the following: –

The motor vehicle accident must be reported to the police within 28 days of the accident.

- An Application for Personal Injury Benefits should be completed within 28 days of the accident but can be completed up to three months after the accident.

- If the insurer makes a decision that affects your ongoing entitlements to statutory benefits, this decision must be internally reviewed within 28 days.

- If you disagree with the insurer’s internal review, you can apply for a Merit Review to SIRA, which must be done within 28 days of receiving the internal review.

- A claim to determine the level of whole person impairment (WPI) should be made within two years from the date of the motor vehicle accident. If your WPI has not been assessed or is less than 10%, then weekly benefits cease two years after the motor vehicle accident.

- A claim for common law damages should be made within three years from the date of the motor vehicle accident. This will allow you to continue to receive weekly payments for up to three years (if your whole person impairment is 10% or less) or for up to a maximum of 5 years (if your whole person impairment is 11% or more).

- A claim to determine your common law damages must be made in PIC within three years from the date of the motor vehicle accident.

These time limits are very strict with limited rights of appeal. The time limits must be strictly complied with otherwise, there may be difficulty making a claim at a later time.

The Lifetime Care & Support Authority of NSW is responsible for administering the Lifetime Care & Support Scheme (“the Scheme”)

The scheme provides lifelong treatment, rehabilitation, and care for people who had sustained catastrophic injuries, including spinal cord injury, moderate to severe brain injury, multiple amputations, serious burns or blindness as a result of a motor vehicle accident.

The Lifetime Care & Support Scheme is also responsible for payment of all medical and care needs for all injured people in car accidents after 1 December 2017 where an insurer has accepted that;

- The injured person was not wholly or mostly at fault and;

- The injured person does not have a minor injury and

- Its five years after the motor vehicle accident

The Lifetime Care & Support Scheme takes over from the insurer after 5 years and is responsible for payment of all ongoing medical and care needs.

Yes.

If you believe the accident was not your fault and you have more than a minor injury, you should always get a lawyer to represent you for a claim under the Motor Accident Injuries Act.

If you deal directly with the insurer yourself, you are likely to get significantly less compensation than if you appoint a lawyer to represent you.

The statistics are telling; in 2010 the average settlement amount for persons injured in a car accident who were not legally represented was about $11,000 in the same period the average settlement amount of those who were legally represented was about $90,000 on average.

If you appoint a lawyer, between 50-70% of the legal costs are also payable by the CTP Insurer.

It makes clear financial sense always to appoint a lawyer to represent you as the insurer pays most of the legal costs, and you will receive a much more significant amount of compensation if you appoint a lawyer.

You should also only use a lawyer who is a Specialist in Personal Injury law as accredited by the Law Society of NSW.

Most lawyers will act on your behalf based on a No Win No Fee Costs Agreement, also called a Conditional Costs agreement.

This means that the lawyer will only be paid legal costs if you are successful in obtaining compensation. If you are not successful, the lawyer will not charge you any legal fees. They may still charge disbursements for the cost of medical reports.

If you are successful in your claim, then part of the legal costs are payable by the CTP insurer in accordance with the Motor Accidents Injuries Regulation NSW 2017.

The CTP insurer pays legal costs based on how far the claim progresses and how much compensation is agreed or awarded to you. This amount is usually 50% of the total legal cost’s payable by you to your lawyer.

Your lawyer is not allowed by the Legal Profession Act to charge an amount or percentage based on what you receive in compensation; this is called Contingency fees and is banned in NSW.

The legal costs and disbursements are payable to your lawyer at the conclusion of your claim.